December 1 2018 is a landmark date in South Korea’s telecom history, the date when it became the first nation to launch 5G services for B2B customers. Four months later, South Korea was also the first to launch mobile 5G services on 3 April 3, 2019, just one hour before Verizon’s 5G launch in the US.

Fast forward to today, let’s look at how 5G is faring in South Korea.

Operators launched B2B first because enterprise clearly was a strategic focus for them. Today, we see how that played out.

Examples of 5G supporting various verticals abound, including SK Telecom’s partnership with Samsung Heavy Industries building a 5G based autonomous navigation system to allow ships to move to a set destination on their own. And KT, for its part, claims 150 B2B use cases with 53 business agreements secured by the end of 2019.

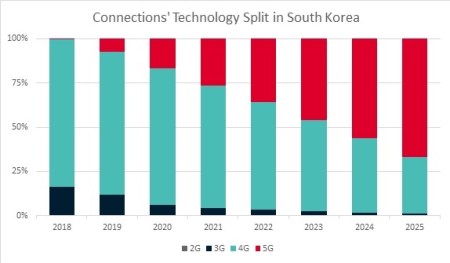

On the consumer front, as of September 2020, 5G connections accounted for around 15 per cent of total mobile connections in the country, crossing the 9 million connections mark. This sets the stage for our estimate of more than 40 million 5G customers by 2025, accounting for 66 per cent of the total connections.

And beyond connections?

Today, 30 per cent of total data traffic is already being routed over 5G networks nearly doubling its stake within one year. LG Uplus reported the average data usage per customer on its 5G network was more than double 4G at 26.8 GB per month at the end of Q1. The 5G launch also helped the market to stabilise declining ARPU at around $25, starting 2019.

South Koreans are known to be early technology adopters. Coupled with handset subsidies and high consumer awareness, we arrived at the following figures for 5G adoption (see chart, below, click to enlarge).

But this is not whole story. The support from the Korean government to provide tax support to domestic operators if they expand nationwide 5G coverage to 70 per cent by 2025 was also a big contributor to rollouts and uptake: capex increased significantly from less than $3 billion from 2015 to 2018, to more than 2015-2018 to more than $4.8 billion in 2019, with a further $4 billion expected in 2020.

This explains the deployment of 115,000 base stations by operators (76 per cent of the total guidance by the government for a complete roll-out) by March.

This is quite Impressive. But what is the result of this investment and impact on consumers?

OpenSignal data on network performance from October shows:

- In Q3, the average 5G download speed was only 5.6-times faster than LTE at 336Mb/s, which is far below the typical rate expected for 5G services.

- Users are able to connect to a 5G network only 22.4 per cent of the time. The availability of 5G is largely limited to Seoul capital region and six metropolitan cities.

While initial uptake has been impressive, the above challenges could have a clear, negative impact on South Korea’s 5G roadmap. Even if consumers aren’t directly impacted, the reputational damage could paint 5G in a negative light. But what can be done to remedy it?

- Commercialisation of mmWave for enterprise use: There is no dearth of narrative on how the full potential of 5G can be realised with the help of enterprise use cases. The demand for 5G capabilities from vertical industries, in turn, could drive wider adoption of mmWave technologies. Unfortunately, the mmWave spectrum (28GHz) acquired by operators in 2018 has not been put to commercial use yet. There is some progress, with all the South Korean operators ordering 5G base stations on this spectrum from Samsung. KT has also started the testing with ultra-reliable low-latency communication (URLLC) technology for latency-sensitive applications including factory automation, autonomous driving and remote surgery. Expediting the progress on 28GHz would help cater to the requirement in various verticals. At the same time, by highlighting the full potential of 5G, enterprise and consumer users will come to see the technology in a better light.

- Launch of standalone: Currently, 5G services are offered on non-standalone networks. The ability of standalone (SA) networks to offer network slicing, or support mission-critical applications with ease will allow operators to work with a wide range of enterprises across verticals. On the consumer side, the use case for SA 5G gets less attention. But if low-latency consumer applications (gaming, AR/VR and so on) are improved, then the result should be a net positive.

- Improve indoor coverage: Coverage being one of the pain areas for customers, action in this direction will help retain existing customers and attract new users. The government plans to deploy around 2,000 indoor 5G base stations, which hopefully should help improve customer satisfaction levels.

- Offer wide range of handsets: Limited availability of compatible devices and high prices can be a deciding factor for consumers to not opt for 5G. Operators should look to partner with multiple manufacturers to offer a wide array of handsets ranging from affordable to premium. These devices, in addition with attractive tariffs, will help maintain strong 5G uptake and set grounds for future.

To sum it all, while 5G has got off to an incredible start in South Korea, there is still much territory to be explored. The commercialisation of 28GHz and SA 5G networks will unlock a wider range of opportunities in the enterprise sector, while addressing coverage and device demands should help to retain and attract customers on 5G.

It will be interesting to see how it all evolves.

– Ankit Sawhney – research manager, and Mansi Goel – research analyst, GSMA Intelligence

The editorial views expressed in this article are solely those of the author and will not necessarily reflect the views of the GSMA, its Members or Associate Members.

Subscribe to our daily newsletter Back

Source of Article